Credit: JLL Belux

Credit: JLL Belux

On Wednesday 26 February 2026, real estate services company JLL unveiled the results of a survey conducted in December 2025 and January 2026 among around 100 real estate investors and developers active in Belgium and Luxembourg.

According to JLL, 2025 marked a recovery in both markets, with transaction volumes rising significantly. In Belgium, total investment volume increased by 42% to €4.5 billion, driven by a record year in logistics and strong retail performance, while the office sector remained under pressure. Luxembourg recorded a nearly 39% increase to €841 million, with an unprecedented sector mix combining office, industrial, shopping centres and residential assets.

Despite this positive momentum, JLL noted that geopolitical uncertainty and its economic impact continue to influence investor sentiment. The survey sought to assess investor positioning in this context.

"In the past 12 months, the European Central Bank (ECB) has reduced its key interest rate several times to reach its current level of 2%. Given that inflation has stabilised around the 2% target, most economists agree that the ECB's monetary policy will remain unchanged in 2026," explained Pierre-Paul Verelst, Head of Research at JLL BeLux. "However, after a decline in long-term interest rates at the end of 2024, they have risen slightly during 2025," he noted.

The survey found that 82% of respondents believe market conditions are stable or improving: 56% consider conditions unchanged compared to the beginning of 2025, while 26% believe they are improving. By contrast, 18% think conditions have deteriorated. Respondents also indicated that banks continue to systematically integrate ESG criteria into financing decisions.

The findings also point to renewed investor confidence, with 88% of respondents either maintaining or increasing their real estate exposure. Some 44% plan to increase exposure, while another 44% foresee no change compared to 2025. A minority (12%) intend to reduce their allocation.

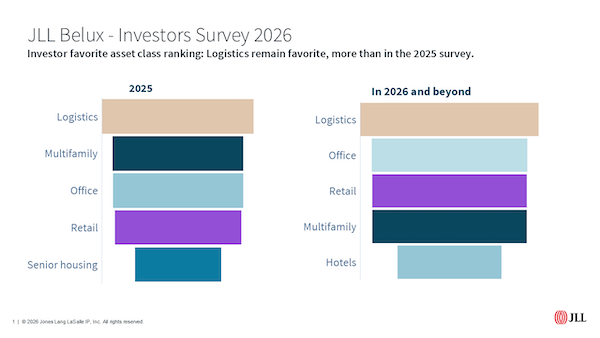

In terms of sector preferences, logistics remained the preferred traditional asset class for both current and future investment. This marks a shift from last year, when multifamily assets were the top choice for 2025 and beyond, although logistics was already the leading asset class at the time. In the latest survey, office real estate ranked second, followed by retail and multifamily. The hotel segment was also gaining interest among investors.

Among alternative asset classes, data centres recorded the strongest increase in preference, cited by 47% of respondents. The segment is gaining momentum partly due to the expansion of artificial intelligence. Student housing also remained highly ranked, having led the previous survey. By contrast, interest in affordable housing declined to 39%, compared to 46% in 2025, which may reflect concerns about government support in a constrained budgetary environment.

Regarding yield expectations, results vary by asset class. In 2025, office yields in Luxembourg fell by 25 basis points to 4.5%, while logistics yields compressed by 10 basis points to 4.9%. For 2026, 46% of investors expect further compression in office yields, particularly in Belgium. Yields stood at 5% in Brussels and 5.75% in Flanders. By contrast, most respondents expect logistics yields (63%) and retail yields (51%) to remain stable.

The survey also identified key risks for the year ahead. In the 2025 edition, Donald Trump’s return to the White House was cited as the most significant risk (76% of respondents). For 2026, political tensions in Europe and internationally remained the primary concern for 69% of investors, followed by economic growth (63%, compared to 48% last year). Although inflation and interest rate risks appear to have stabilised, 47% of respondents continue to monitor these factors closely.

Looking ahead to 2026, JLL noted that while recent turbulence related to American tariff policy and tensions in the Middle East calls for caution, recent reference transactions are providing greater visibility on achievable resale returns.

"The conditions are therefore in place to restore liquidity in all segments," affirmed Vincent Van Brée, Head of Capital Markets at JLL BeLux. "We expect a good year for both office and shopping centres. The hospitality segment also looks very promising," he concluded.