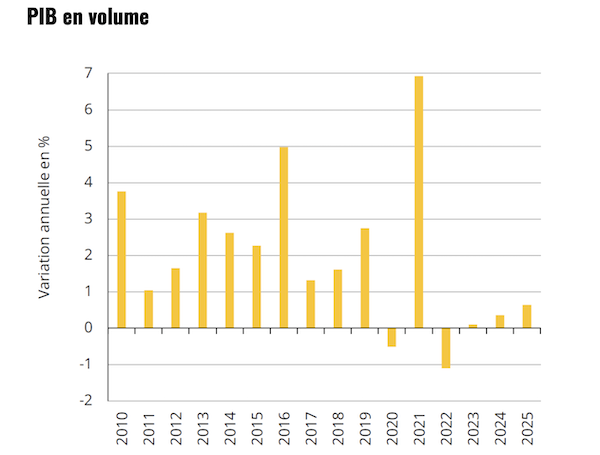

GDP (PIB en volume);

Credit: STATEC

GDP (PIB en volume);

Credit: STATEC

On Tuesday 24 March 2026, STATEC published its latest Conjoncture Flash report, indicating that Luxembourg’s GDP growth stalled at the end of 2025, with a slight quarterly decline and annual growth remaining weak at 0.6%, amid growing uncertainty linked to the international environment and rising inflation risks.

According to the report, Luxembourg’s real GDP stalled in the final quarter of 2025 after four consecutive quarters of growth, recording a slight decline of 0.1% quarter-on-quarter.

This quasi-stagnation reflected contrasting trends across sectors. Positive contributions came mainly from non-market activities, including public administration, education and health, as well as industry and, to a lesser extent, business services. In contrast, most other market sectors saw a decline in value added in the fourth quarter, with the most negative impacts coming from information and communication services, trade, transport and financial activities. The decline in financial activities (-0.3%) followed a sharp rebound in the previous quarter (+2.7%).

As in the third quarter of 2025, consumer spending (private and public) continued to grow at a relatively dynamic pace, driven in particular by expenditure on health, telecommunications and catering services, while purchases of private vehicles declined. Investment expenditure fell by 11.5% quarter-on-quarter, following a particularly strong increase in the third quarter linked mainly to satellite acquisitions. Total exports declined by around 1% quarter-on-quarter, mainly due to non-financial services, while exports of financial services increased for the second consecutive quarter.

Overall, GDP growth reached 0.6% for 2025, according to STATEC, marking a slight acceleration compared to 2023 and 2024, but remaining well below historical averages. STATEC had previously projected growth of 1.0% for 2025 in its latest forecasts.

Assets of collective investment undertakings in Luxembourg increased by 6.5% year-on-year in 2025, reflecting a rise in net fund inflows. This growth was mainly driven by higher net inflows into bond and money market funds, supported by falling interest rates, and, to a lesser extent, into equity funds, reflecting stock market performance. Ireland recorded the strongest growth in net issues in Europe in 2025 (€436 billion, compared with €244 billion in Luxembourg), around half of which was in index funds (ETFs). As a result, Ireland’s market share rose by 0.5 percentage points to 22% of European assets under management, while Luxembourg’s share declined slightly to 25%. Germany, the United Kingdom and the Netherlands also saw their market shares decrease.

Rising geopolitical tensions at the start of 2026 led to volatility in financial markets in March, which is expected to weigh on valuations and net inflows into funds at the end of the first quarter.

Bank results in Luxembourg were dampened by falling interest margins in 2025. Net profit declined by 5.4% (or 3.6% excluding provisions and taxes), mainly due to a reduction in interest margins following falling interest rates since mid-2024. Margins fell by 3% year-on-year, although they remain around twice as high as in 2021, before the rate-hiking cycle. The margin rate also increased from 0.15% to 0.30%. Net commission income recorded modest growth (+2.2% year-on-year in the first half of the year), driven mainly by custodian banks for investment funds, supported by strong fund performance.

According to the CSSF, “Due to a break in the series caused by the merger of two banks, which affected the figures for the first quarter of 2024, the relative changes in general expense items are significantly overestimated”.

In the eurozone, net banking income in the first three quarters of 2025 showed mixed trends, increasing in half of the countries and declining in the other half, leaving the overall result broadly unchanged. Net interest margins declined in three-quarters of member states, falling by 4.3% overall.

Employment growth in Luxembourg strengthened in the second half of 2025, bringing the annual increase to 1.2%, while growth in the eurozone slowed slightly to 0.7%. This was driven mainly by an upturn in non-market services, particularly healthcare, and a less pronounced decline in construction. In contrast, sectors such as trade, transport, hospitality, ICT and, to a lesser extent, financial services lost momentum. Notably, employment in ICT declined, marking the first drop since 2003, when the sector had grown by around 4% on average per year.

Labour cost growth slowed in the fourth quarter of 2025. Compensation per employee rose by around 4% year-on-year, down from 5.4% in the previous quarter, mainly due to lower bonuses and gratuities. Over the full year, compensation increased by 4.4%, compared to 3.5% in 2024, with around 40% of this rise linked to indexation and wage increases, and a further 20% to higher employer contributions. Similar trends were observed across the eurozone, although developments varied by country.

STATEC also highlighted rising price pressures linked to geopolitical tensions. Following the closure of the Strait of Hormuz, energy and commodity prices increased sharply, with diesel prices in Luxembourg rising by around €0.54 (37%) and 95-octane petrol by €0.24 (16%) since the end of February. Fertiliser and semiconductor prices have also increased significantly, raising concerns about broader inflationary effects. While STATEC is maintaining its forecast for the next indexation in the second quarter of 2026, it warned that prolonged disruption could further fuel inflation.

The full report is available on the STATEC website.